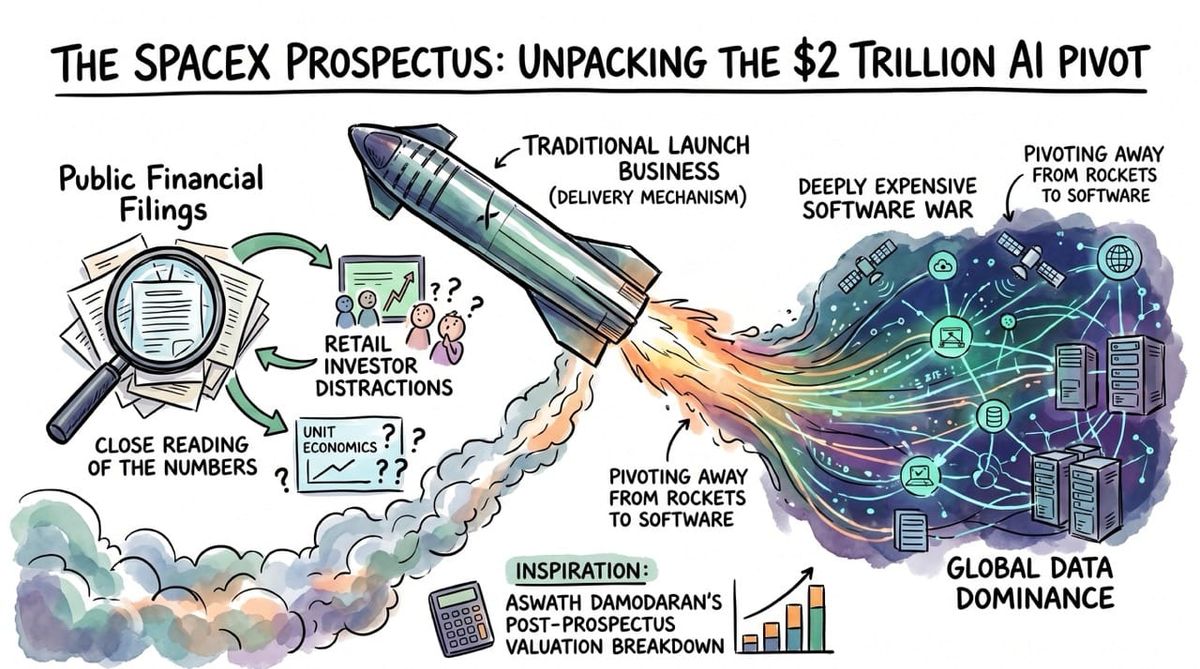

The SpaceX Prospectus: Aswath Damodaran Unpacking the Two Trillion Dollar AI Pivot

Everyone assumes the SpaceX public offering is about colonizing Mars. The actual financial data reveals it is a highly leveraged bet on enterprise artificial intelligence and satellite connectivity.

Public financial filings are frequently designed to distract retail investors from the underlying unit economics. A close reading of the actual numbers reveals a company rapidly pivoting away from rockets to fund a deeply expensive software war.

Inspiration: Analyzing the post prospectus valuation breakdown by Aswath Damodaran. Realizing the traditional space launch business is simply a delivery mechanism for a much broader strategy involving global data dominance.

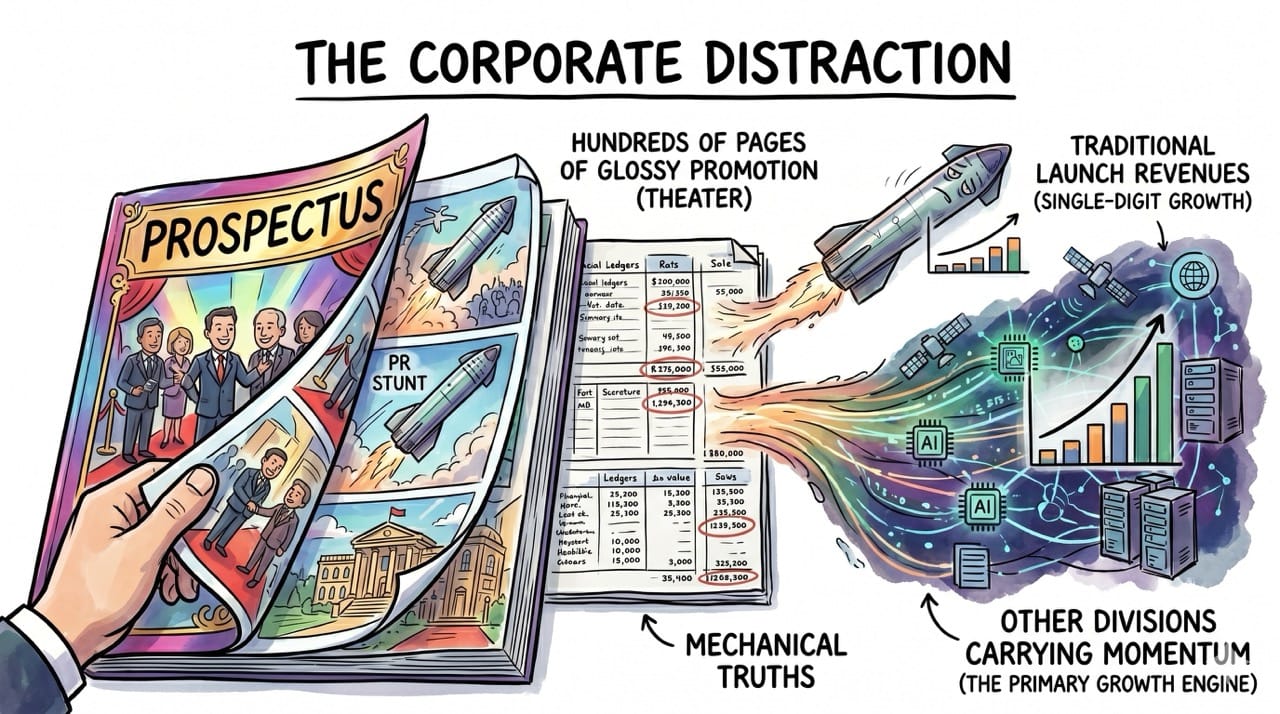

The Corporate Distraction

Financial documents for modern public offerings are largely theater designed to overwhelm investors with hundreds of pages of glossy photos.

You have to actively ignore the promotional material to find the actual mechanical truths hiding underneath.

The numbers clearly show that the traditional space launch business is no longer the primary growth engine.

Launch revenues are only growing in the single digits while other divisions completely carry the corporate momentum.

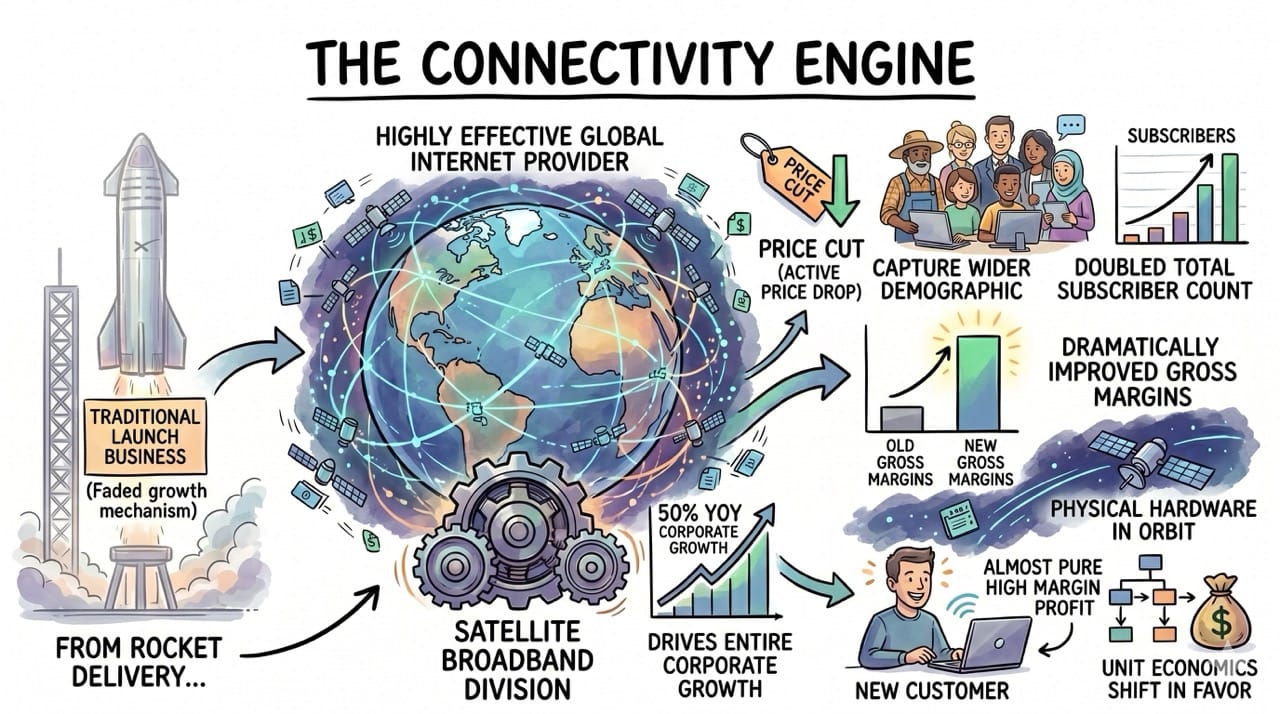

The Connectivity Engine

The company has quietly transitioned into a highly effective global internet provider.

The satellite broadband division is currently driving the entire corporate growth rate at fifty percent year over year.

They are actively dropping the monthly subscription price to capture a significantly wider consumer demographic.

This strategy successfully doubled their total subscriber count and dramatically improved their baseline gross margins.

Once the physical hardware is orbiting the earth the unit economics completely shift in their favor.

Every new internet customer they acquire represents almost pure high margin profit.

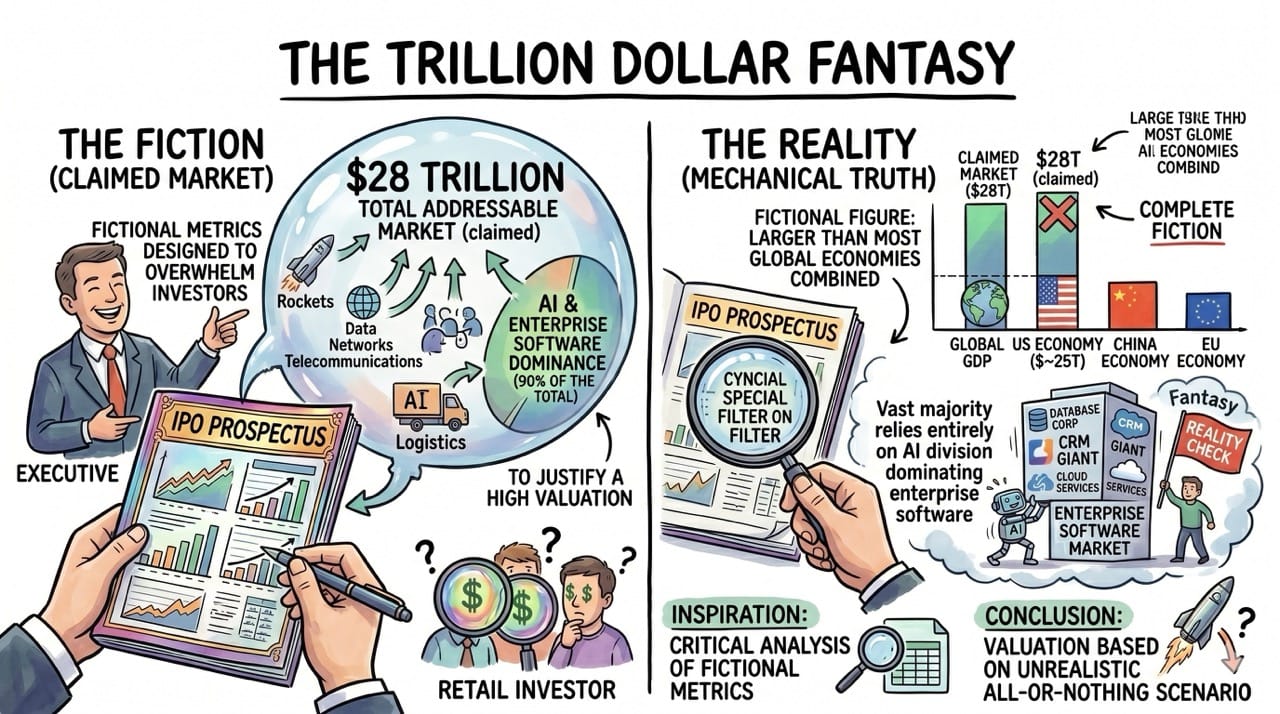

The Trillion Dollar Fantasy

Technology companies frequently invent fictional metrics to justify high valuations during a public debut.

The prospectus claims a total addressable market of twenty eight trillion dollars across all their business lines.

This specific number is complete fiction and represents a figure larger than most global economies combined.

The vast majority of this projected market relies entirely on their artificial intelligence division dominating enterprise software.

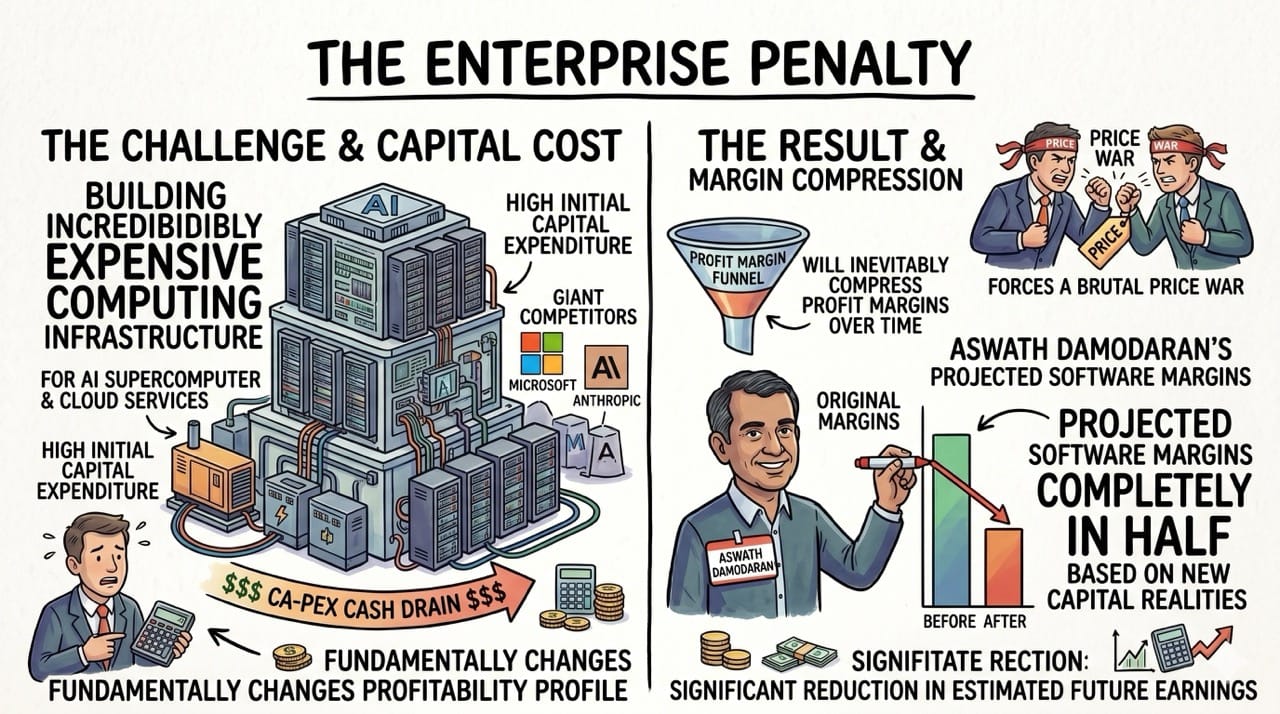

The Enterprise Penalty

Competing in the enterprise artificial intelligence sector fundamentally changes the profitability profile of the entire company.

Serving corporate clients requires building incredibly expensive computing infrastructure to effectively compete with Microsoft and Anthropic.

This aggressive expansion forces them into a brutal price war that will inevitably compress their profit margins over time.

Damodaran cut his projected operating margins for their software division completely in half based on these new capital realities.

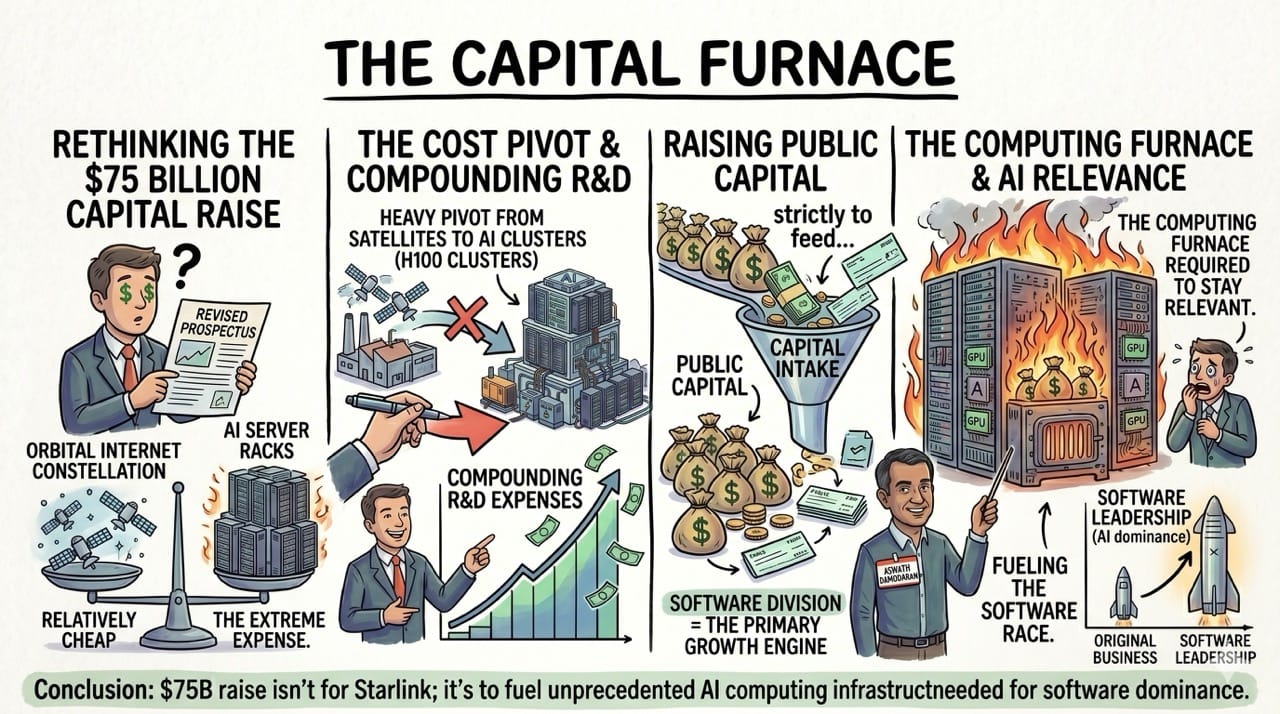

The Capital Furnace

The financial narrative requires us to rethink why they actually need to raise seventy five billion dollars right now.

Building an orbital internet constellation is relatively cheap compared to building physical server farms for artificial intelligence.

Their research and development expenses are compounding rapidly as they pivot toward heavy algorithmic processing.

They are raising public capital strictly to feed the computing furnace required to stay relevant in the software race.

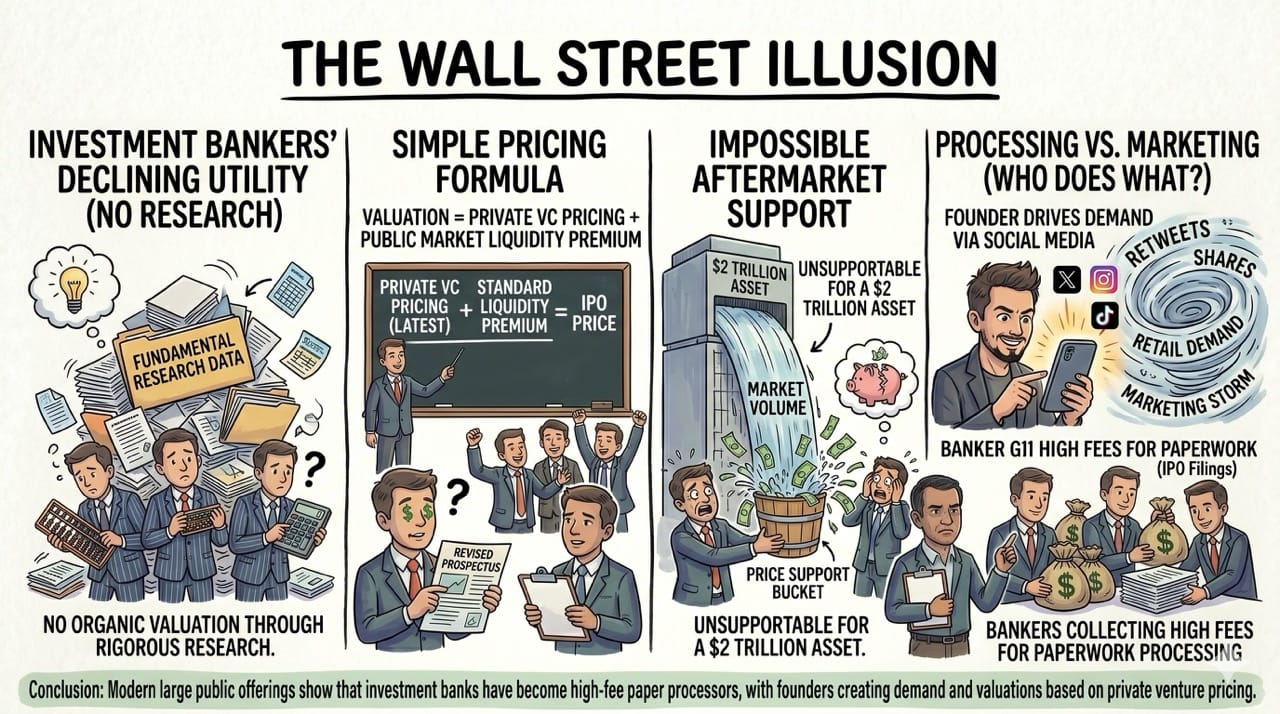

The Wall Street Illusion

This specific public offering exposes the rapidly declining utility of traditional investment banks.

The bankers did not organically discover the valuation for this company through rigorous fundamental research.

They simply took the latest private venture capital pricing and added a standard premium for public market liquidity.

Furthermore they cannot provide traditional aftermarket price support for a two trillion dollar asset.

The bankers are simply collecting high fees to process paperwork.

The founder is driving all the actual marketing and retail demand through his own social media accounts.

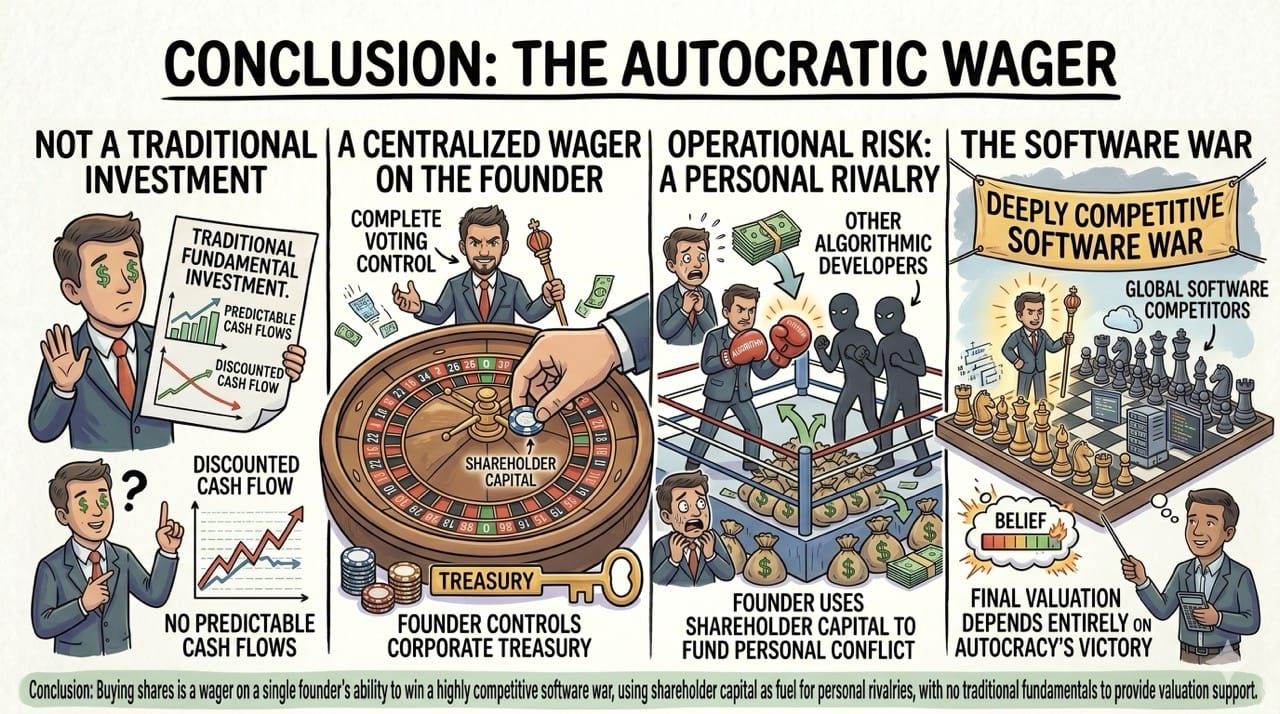

Conclusion: The Autocratic Wager

Buying shares in this company is not a traditional fundamental investment based on predictable cash flows.

It is a highly centralized wager on a single founder holding complete voting control over the corporate treasury.

The real operational risk is that the founder uses shareholder capital to fund a personal rivalry against other algorithmic developers.

The final valuation depends entirely on whether you believe this specific autocracy can win a deeply competitive software war.