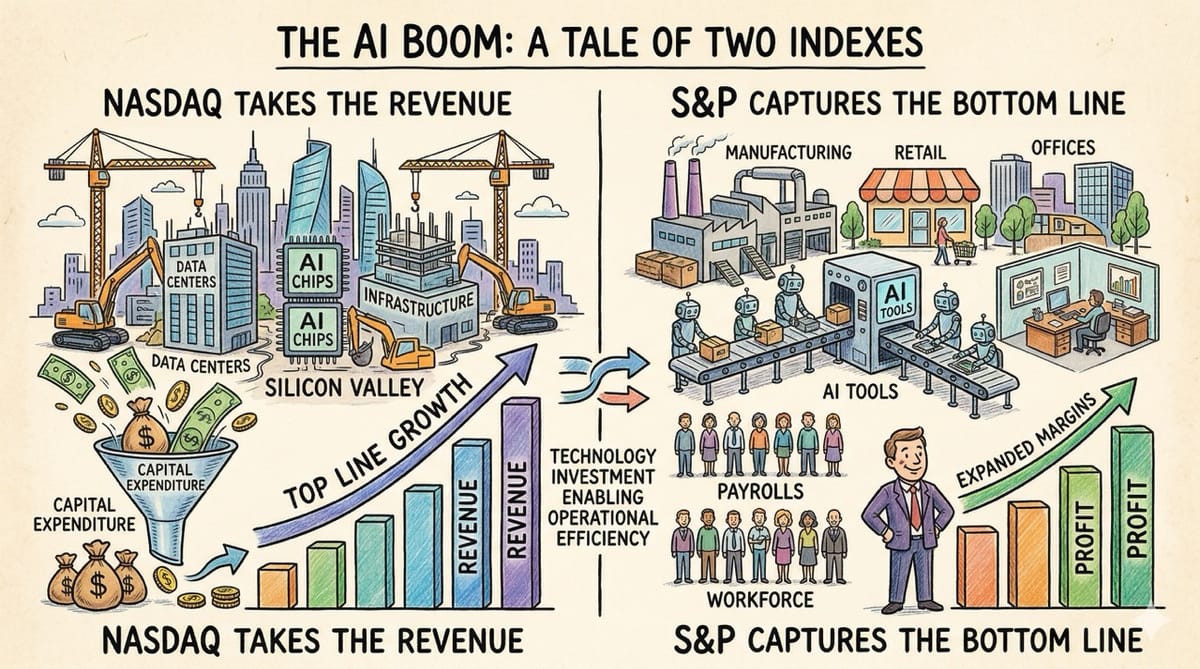

The AI Boom: Nasdaq Takes the Revenue, S&P Captures the Bottom Line

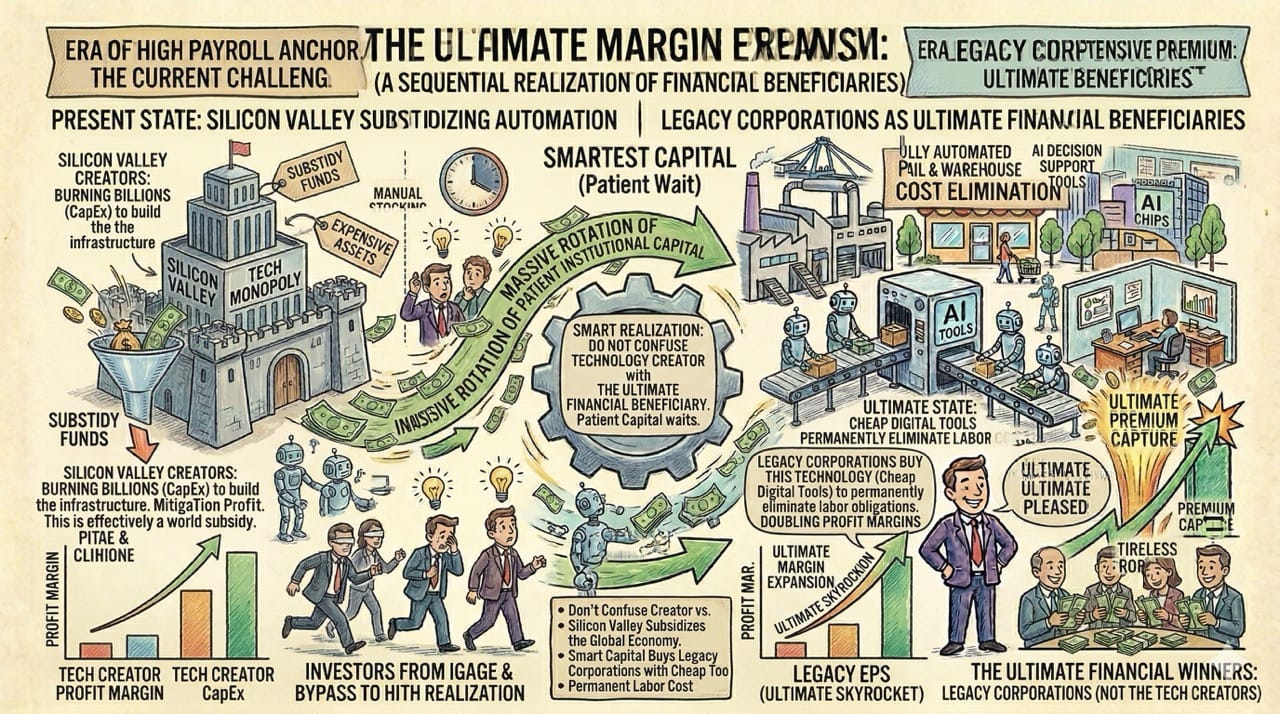

We assume the artificial intelligence revolution will strictly enrich the major technology monopolies building the foundational models. In reality, the most massive explosion of corporate profit margins will belong to legacy, labor intensive companies outside of Silicon Valley.

Silicon Valley is spending billions on infrastructure to generate top line growth. The broader market will simply use those tools to ruthlessly slash their payrolls and expand their profit margins.

Inspiration: Analyzing the massive capital expenditure budgets of major technology companies compared to the rising productivity metrics across traditional industries. Realizing that the ultimate financial winners of artificial intelligence will be the legacy corporations that successfully automate their massive human workforces.

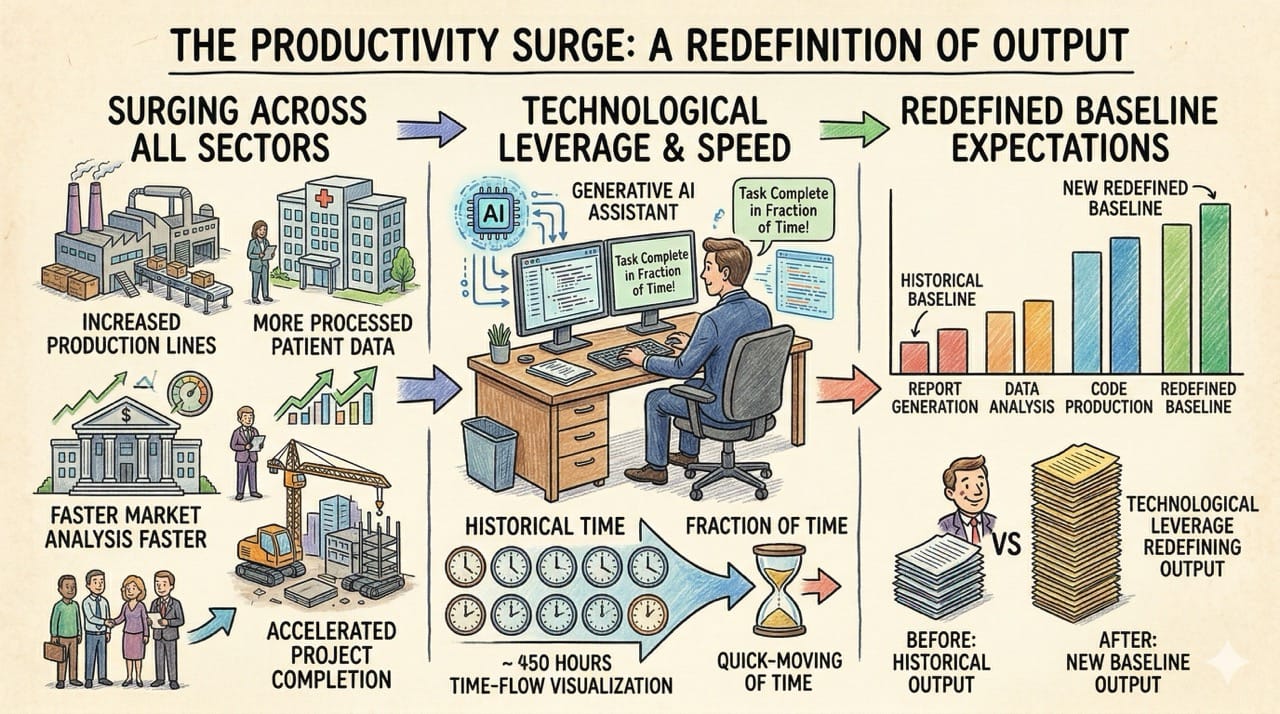

The Productivity Surge

Worker productivity is currently surging across virtually every sector of the global economy.

Employees are utilizing generative software to execute complex tasks in a fraction of the historical time required.

This technological leverage is completely redefining the baseline output expectations for the modern corporate worker.

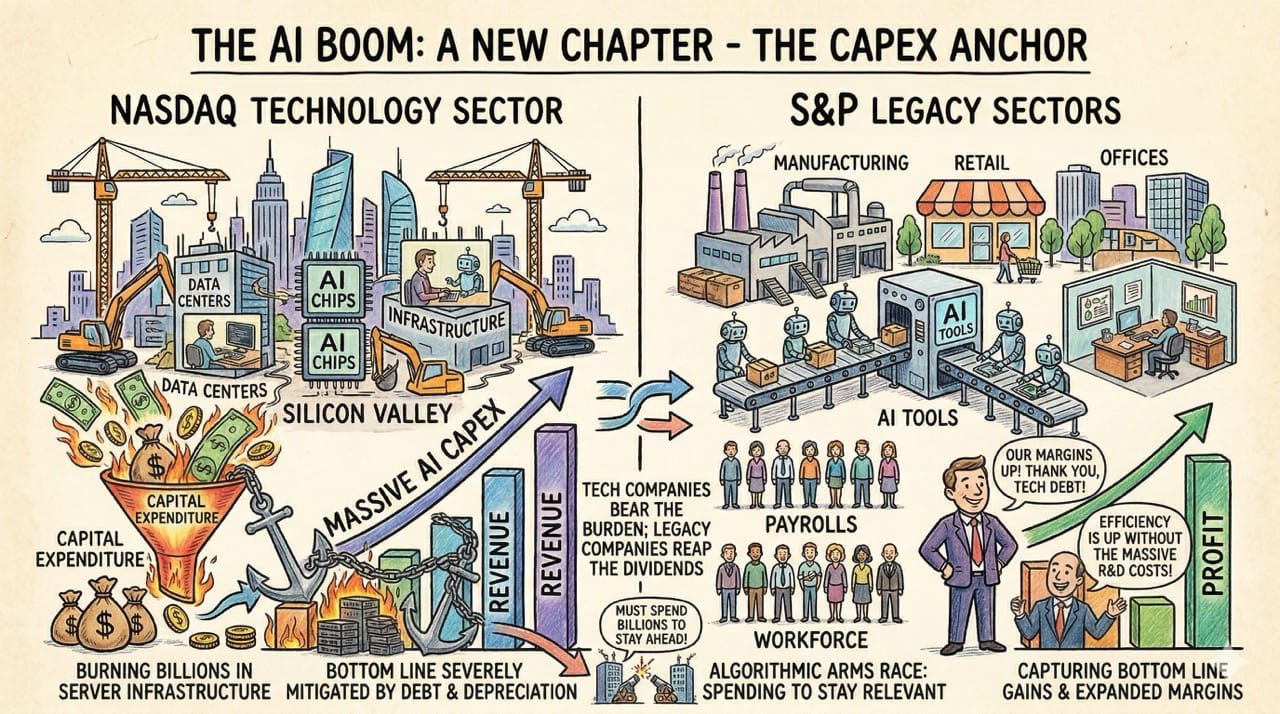

The CapEx Anchor

Technology companies are certainly experiencing these exact same internal productivity gains.

However, their massive capital expenditure budgets required to build artificial intelligence data centers will severely mitigate their actual bottom line.

They are burning billions of dollars on server infrastructure just to stay relevant in the current algorithmic arms race.

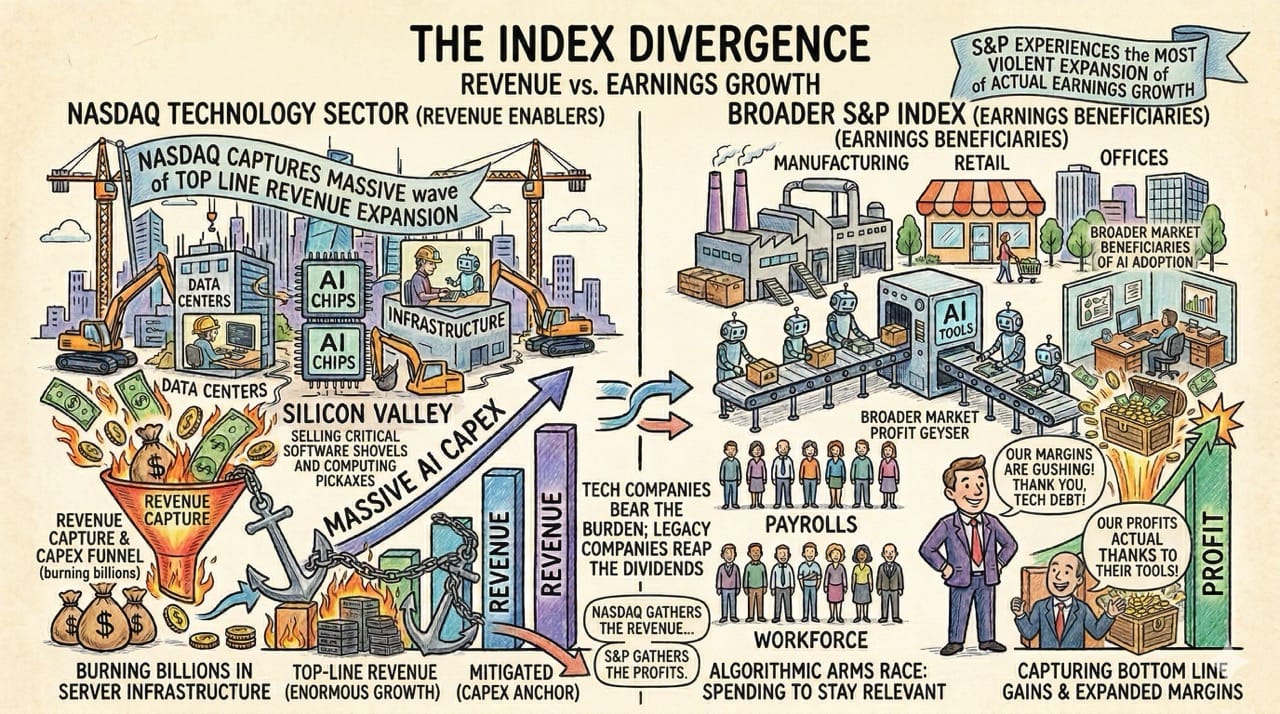

The Index Divergence

The Nasdaq index will absolutely capture the massive wave of top line revenue expansion.

They are successfully selling the critical software shovels and computing pickaxes for this modern digital gold rush.

However, the most violent expansion of actual earnings growth will occur within the broader S&P index.

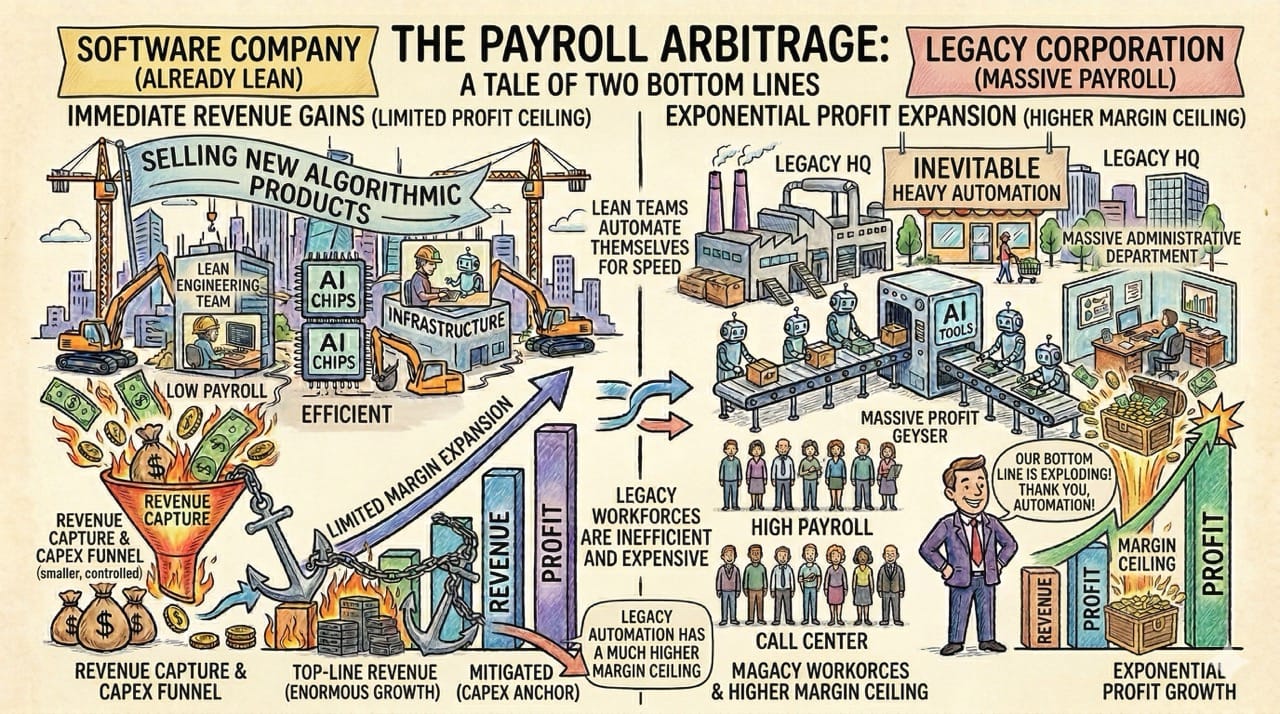

The Payroll Arbitrage

A software company with an already lean engineering team will see immediate revenue gains from selling new algorithmic products.

Conversely, a legacy corporation with a massive administrative and logistics department possesses a much higher margin ceiling.

When those large teams inevitably become heavily automated, the corporate bottom line will expand exponentially.

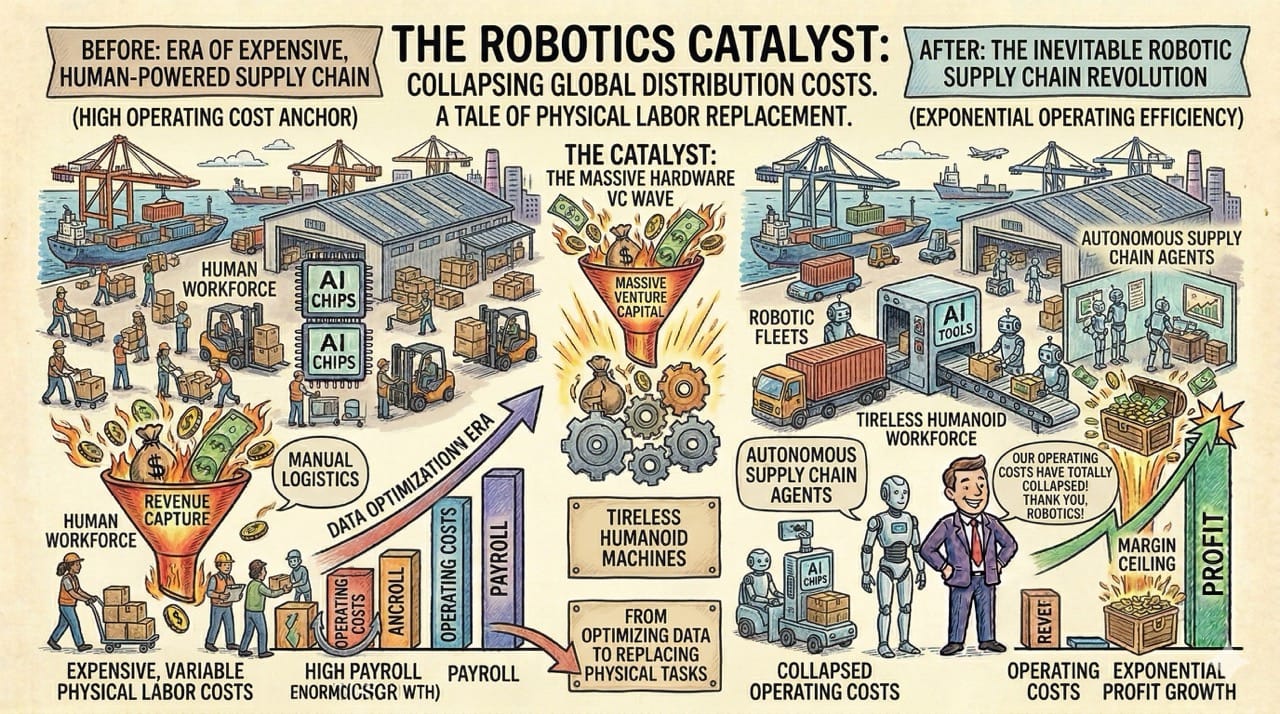

The Robotics Catalyst

We must also factor in the upcoming wave of physical robotics and autonomous supply chain agents.

Massive venture capital is currently flowing into hardware projects designed to replace expensive physical labor with tireless humanoid machines.

As these robotic fleets come online, the traditional operating costs of global distribution will completely collapse.

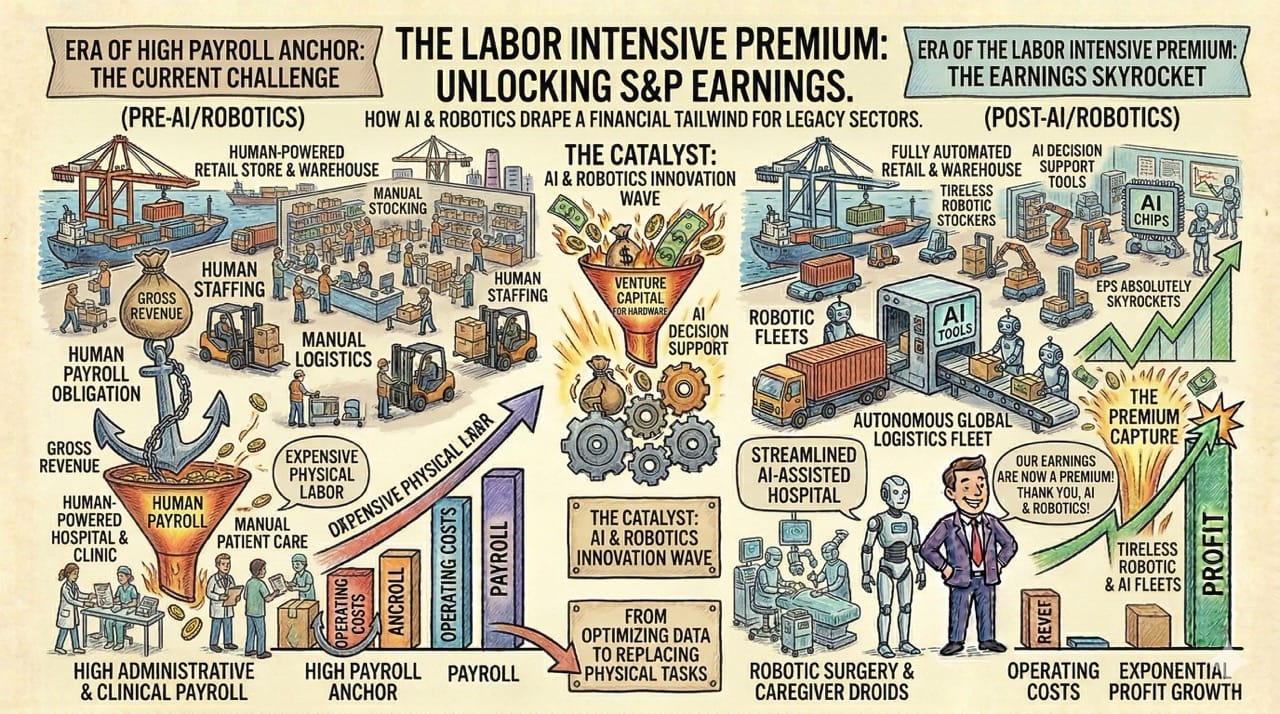

The Labor Intensive Premium

This dynamic creates a massive financial tailwind for highly labor intensive companies that dominate the traditional S&P listings.

Retailers, shipping firms, and legacy healthcare providers currently spend the vast majority of their gross revenue on human payroll.

When artificial intelligence and physical robotics drastically reduce those payroll obligations, their earnings per share will absolutely skyrocket.

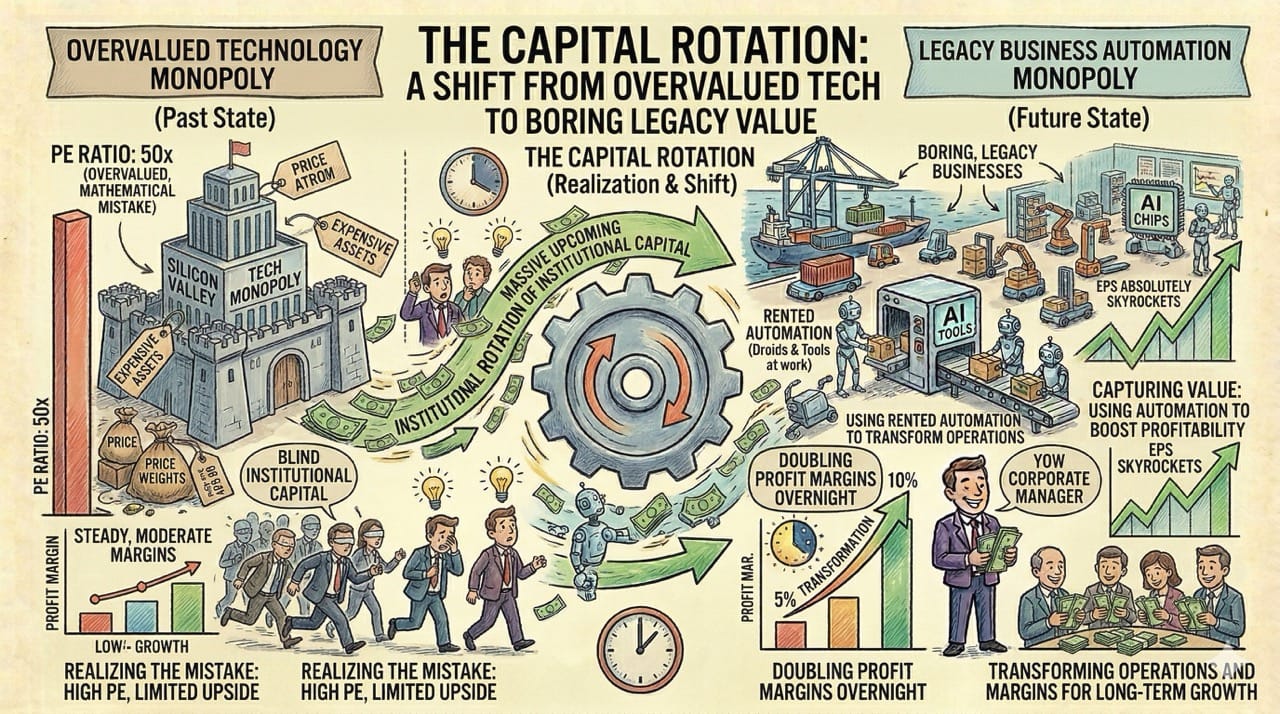

The Capital Rotation

This guarantees a massive upcoming rotation of institutional capital.

Investors will eventually realize that buying an expensive technology monopoly at fifty times earnings is a mathematical mistake.

They will rotate heavily into boring, legacy businesses that are quietly using rented automation to double their profit margins overnight.

Conclusion: The Ultimate Margin Expansion

Do not confuse the creator of a technology with the ultimate financial beneficiary of that technology.

Silicon Valley is currently subsidizing the automation of the entire global economy.

The smartest capital will patiently wait to buy the legacy corporations that use these cheap digital tools to permanently eliminate their labor costs.