The Clean Data Fed: Why the Next Chairman Will Force Wall Street to Upgrade Its Plumbing

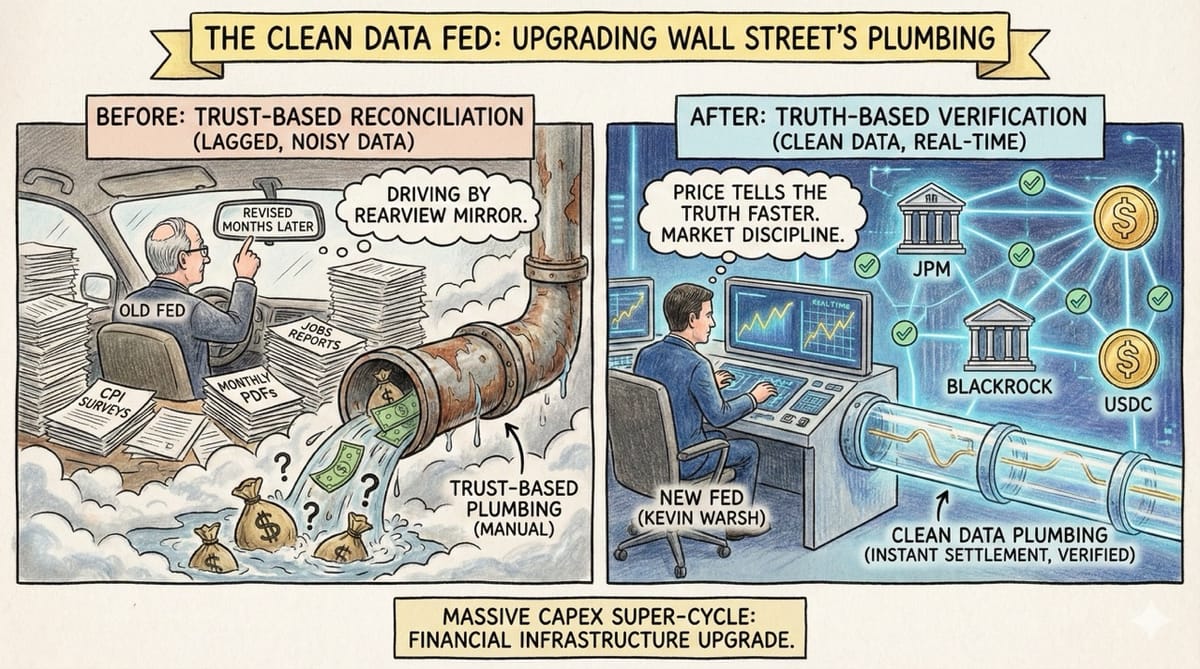

The Fed has always driven the economy by looking in the rearview mirror. Kevin Warsh wants to install a GPS. This shift to "Clean Data" will trigger a massive CapEx super-cycle for the companies that modernize Wall Street's plumbing.

We are moving from a system of "Trust-Based Reconciliation" to "Truth-Based Verification." The companies building the new rails are about to become the most valuable utilities in finance.

Inspiration: Reading about Kevin Warsh’s philosophy on "Market Discipline" and realizing that you can't have discipline without data transparency.

The nomination of Kevin Warsh as Chairman of the Federal Reserve is not just a personnel change; it is a regime change.

For decades, the Fed has operated on lagged, noisy data. They rely on surveys (like the CPI or Jobs Report) that are often revised months later.

Effectively, the most powerful economic institution in the world drives the economy by looking in the rearview mirror.

Warsh represents a different philosophy.

He believes in Market Signals. He has argued that price tells the truth faster than a bureaucrat.

To implement this doctrine, he needs "Clean Data." He cannot rely on monthly PDFs. He needs a financial system that reports in real-time, settles instantly, and verifies mathematically.

This triggers a massive CapEx Super-Cycle for the financial infrastructure of the US. Banks, asset managers, and stablecoin issuers will be forced to upgrade their plumbing to meet this new standard of fidelity.

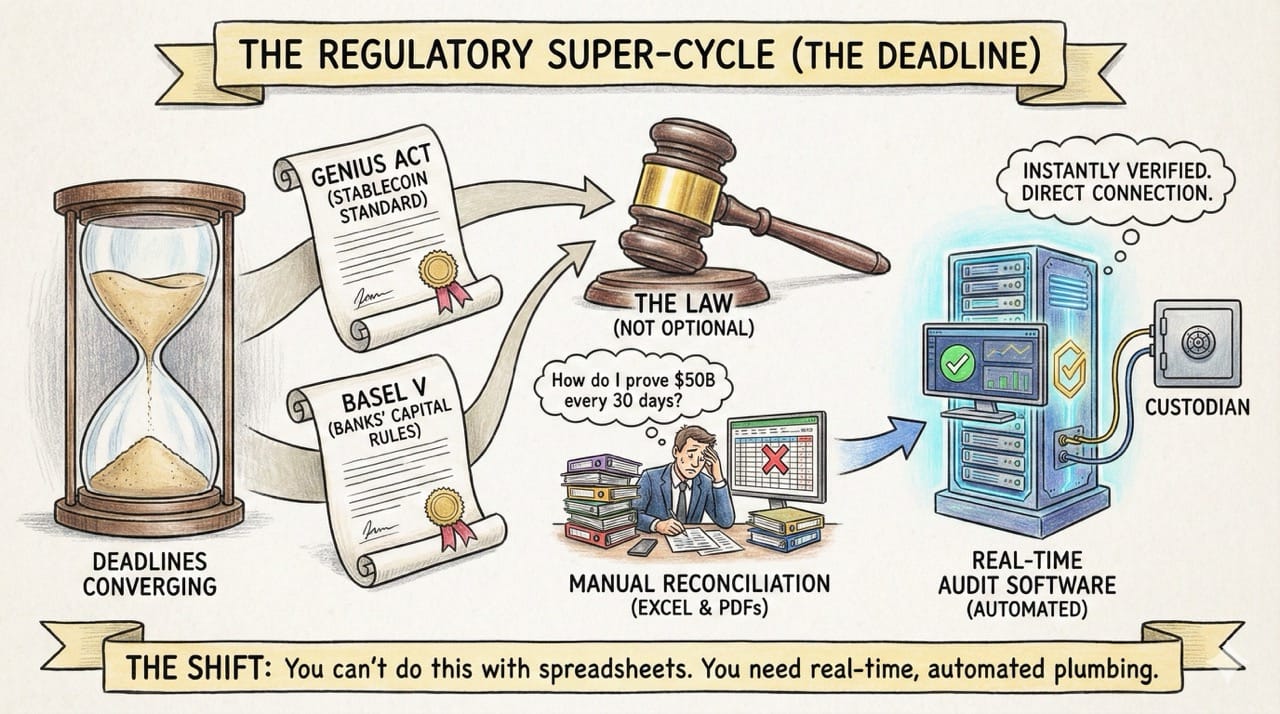

The Regulatory Super-Cycle (The Deadline)

This isn't optional. It’s the law. Two massive regulatory deadlines are converging to force this upgrade.

1. The GENIUS Act (The Stablecoin Standard): This act legalizes private stablecoins but mandates 1:1 reserves with short-term Treasuries. Crucially, it requires monthly attestations examined by registered accounting firms.

The Shift: You can't do this with Excel spreadsheets and manual reconciliation. To prove you have $50B in Treasuries every 30 days, you need automated, real-time audit software that connects directly to custodians.

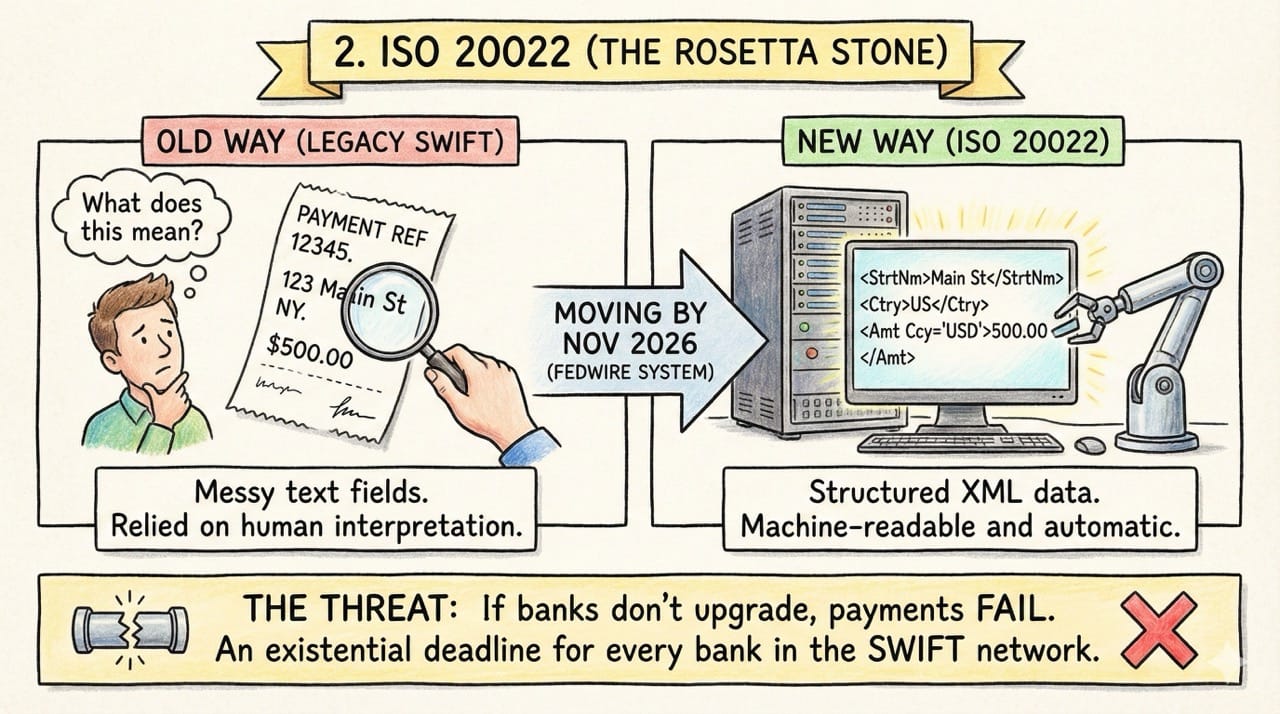

2. ISO 20022 (The Rosetta Stone): By November 2026, the Fedwire system moves to ISO 20022.

- Old Way (Legacy SWIFT): Messy text fields. "123 Main St NY." It relied on humans to interpret the data.

- New Way (ISO 20022): Structured XML data.

<StrtNm>Main St</StrtNm>. It allows machines to read and process payments automatically. - The Threat: If banks don't upgrade their plumbing to handle this rich data, their payments will fail. It is an existential deadline for every bank in the swift network.

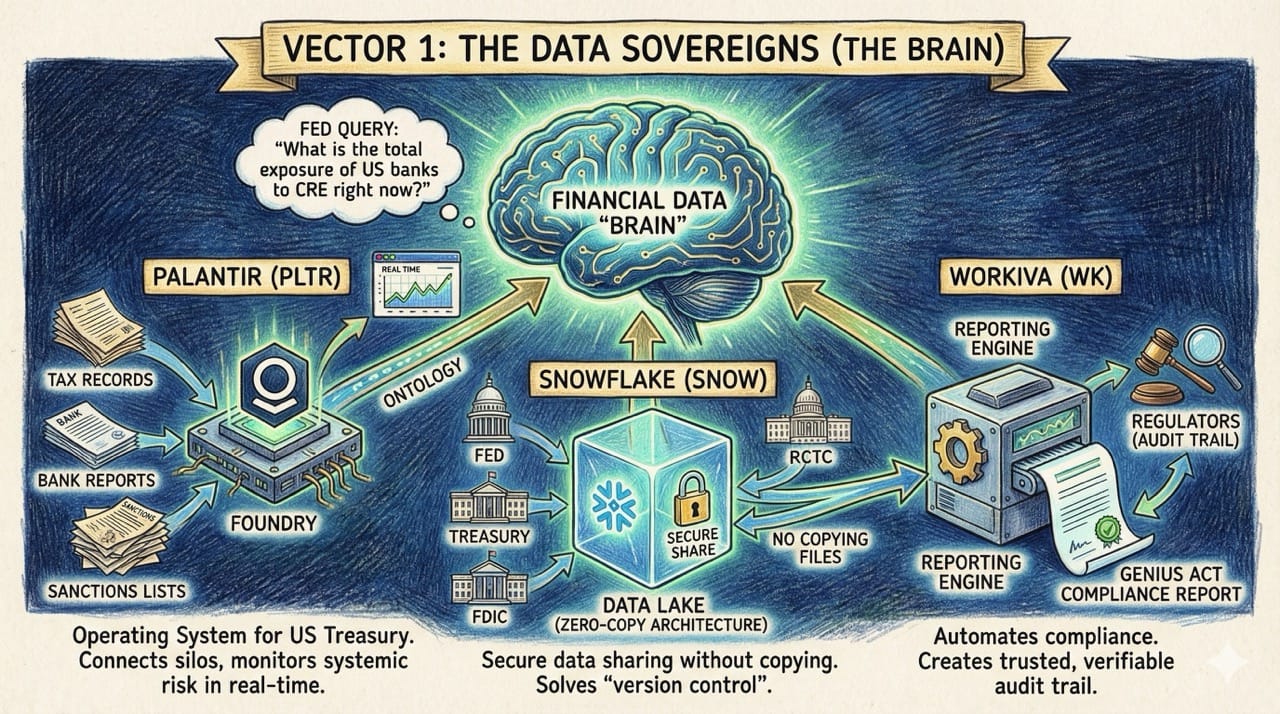

Vector 1: The Data Sovereigns (The Brain)

Who benefits? The companies that provide the "Brain" to ingest, clean, and analyze this massive influx of data.

- Palantir (PLTR): They are becoming the operating system for the US Treasury. Their "Foundry" platform connects disparate data silos (tax records, bank reports, sanctions lists) into a single "Ontology." If the Fed wants to monitor systemic risk in real-time (e.g., "What is the total exposure of US banks to commercial real estate right now?"), they will likely use Foundry.

- Snowflake (SNOW): The data lake. Their "Zero-Copy Architecture" is critical. It allows agencies (Fed, Treasury, FDIC) to share data securely without copying files back and forth. This solves the "version control" problem of government data.

- Workiva (WK): The reporting engine. They automate the compliance reports for the GENIUS Act. They connect the data source directly to the final report, creating an audit trail that regulators trust.

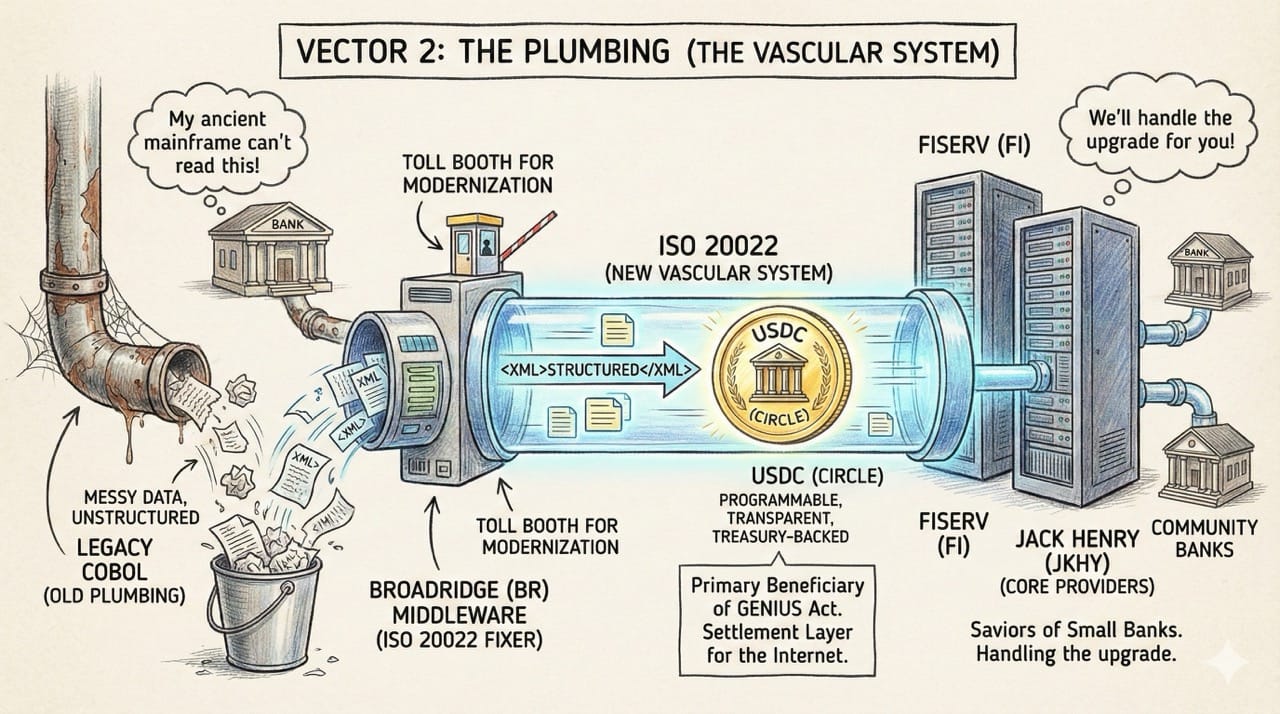

Vector 2: The Plumbing (The Vascular System)

This vector covers the "pipes" that move money and messages. If the data is clean, the pipes need to be wide enough to carry it.

- Broadridge (BR): The "ISO 20022 Fixer." Most banks run on ancient COBOL mainframes that can't read XML. Broadridge provides the middleware that allows old bank systems to talk to the new Fedwire. They are the toll booth for modernization.

- Circle (CRCL): The primary beneficiary of the GENIUS Act. By essentially becoming a "Narrow Bank" backed by Treasuries, USDC becomes the settlement layer for the internet. It is the "cleanest" dollar because it is programmable and transparent.

- Fiserv (FI) & Jack Henry (JKHY): The saviors of the small banks. Community banks can't build their own ISO 20022 solutions. They will rely on these core providers to handle the upgrade for them.

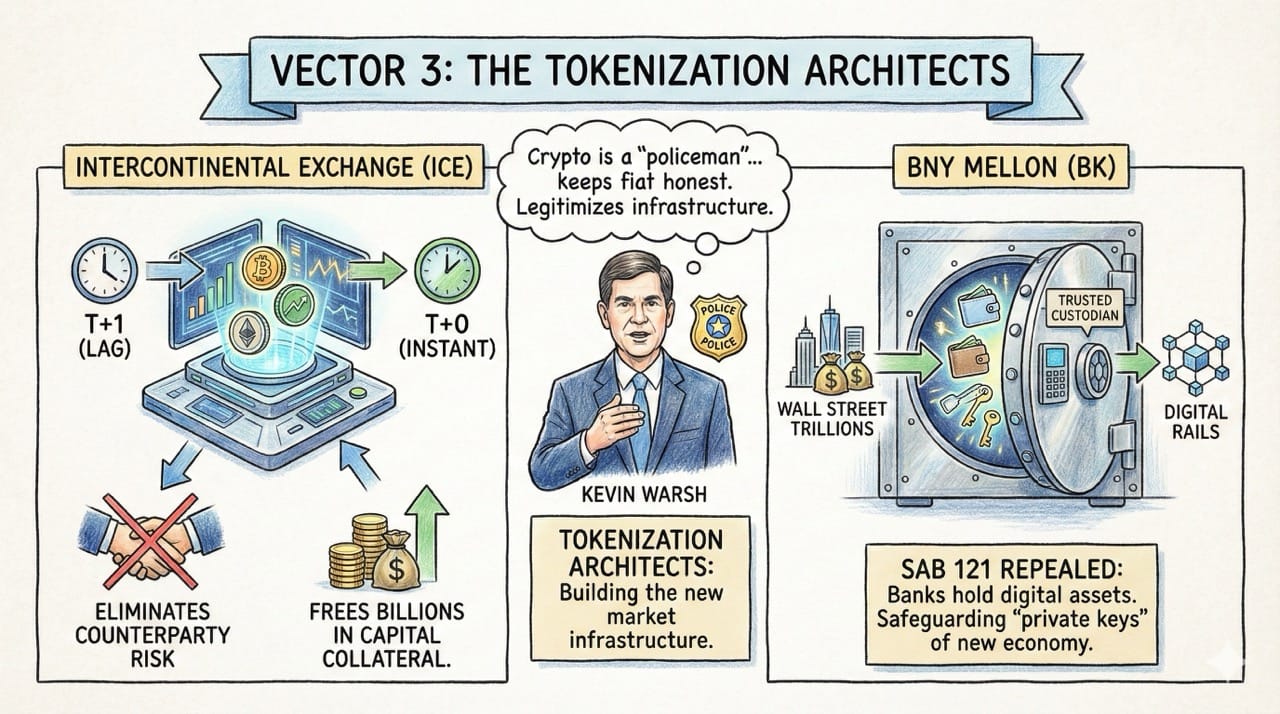

Vector 3: The Tokenization Architects

Warsh isn't hostile to crypto; he views it as a "policeman"—a market signal that keeps fiat honest. This legitimizes the infrastructure of digital assets.

- Intercontinental Exchange (ICE): The owner of the NYSE. They are building a platform for trading tokenized assets. This moves settlement from T+1 (one day lag) to T+0 (instant). It eliminates counterparty risk and frees up billions in capital collateral.

- BNY Mellon (BK): The custodian. With the repeal of SAB 121 (implied by the new regime), banks can finally hold digital assets on their balance sheets. BNY becomes the bridge between Wall Street trillions and digital rails, safeguarding the "private keys" of the new economy.

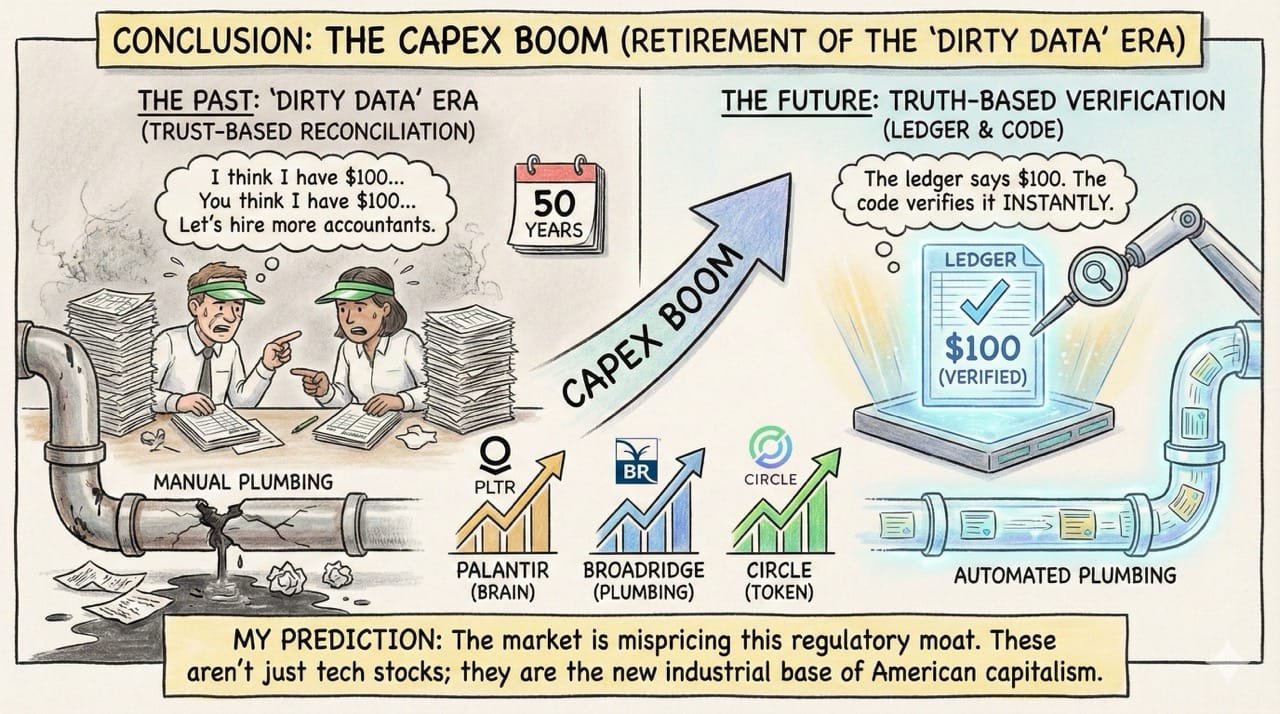

Conclusion: The CapEx Boom

We are witnessing the retirement of the "Dirty Data" era.

For 50 years, finance ran on "Trust-Based Reconciliation"—I think I have $100, you think I have $100, and we hire accountants to agree. We are moving to "Truth-Based Verification"—the ledger says I have $100, and the code verifies it instantly.

My Prediction: The market is mispricing this regulatory moat. As the Fed moves to automate supervision, the companies providing the requisite data fidelity—Palantir, Broadridge, Circle—will command a premium valuation. They aren't just tech stocks; they are the new industrial base of American capitalism.