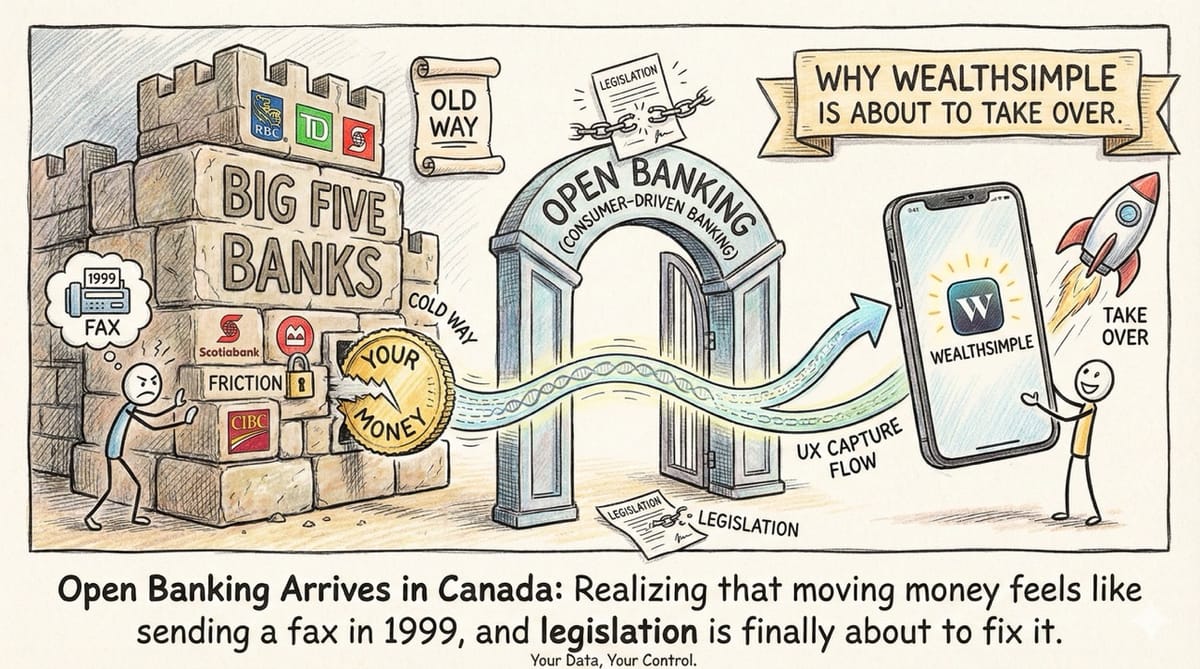

Open Banking Arrives in Canada: Why Wealthsimple Is About to Take Over

Canada’s banking monopoly is about to break. Open Banking gives consumers ownership of their financial data. This is an existential threat to the Big Five and a rocket ship for Wealthsimple.

The Big Five banks have relied on friction to keep your money. Open Banking removes the friction. Wealthsimple has the UX to capture the flow.

Inspiration: Realizing that moving money between Canadian banks feels like sending a fax in 1999, and that legislation is finally about to fix it.

Canada has one of the most protected banking oligopolies in the world. The Big Five (RBC, TD, Scotiabank, BMO, CIBC) control everything.

But the government just signaled the arrival of Consumer-Driven Banking (Open Banking). This means you own your financial data, not the bank. You can grant a third-party app read/write access to your accounts instantly.

This changes the physics of Canadian finance.

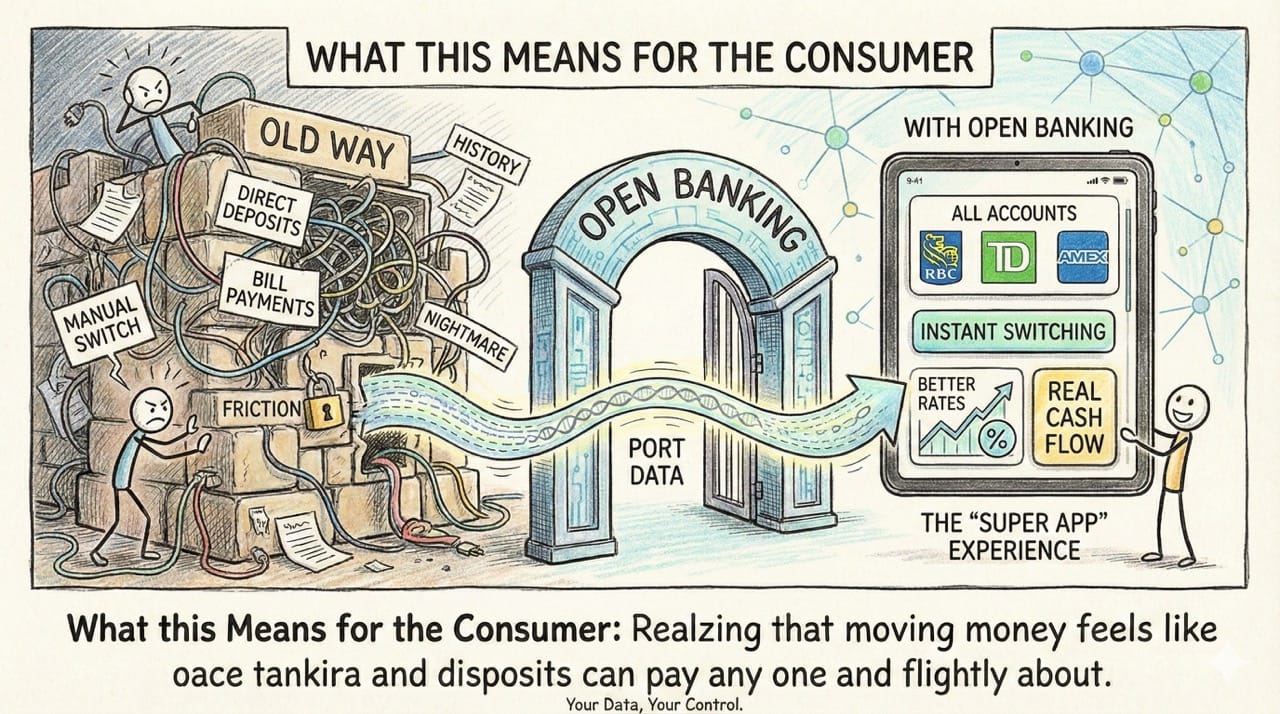

What This Means for the Consumer

Right now, if you want to switch banks, it’s a nightmare. You have to move direct deposits, bill payments, and history manually. With Open Banking:

- Instant Switching: You can port your data to a new provider in seconds.

- The "Super App": You can see all your accounts (RBC Chequing, TD Mortgage, Amex Credit) in one dashboard.

- Better Rates: Lenders can see your real cash flow instantly, offering competitive loans without a credit check ping.

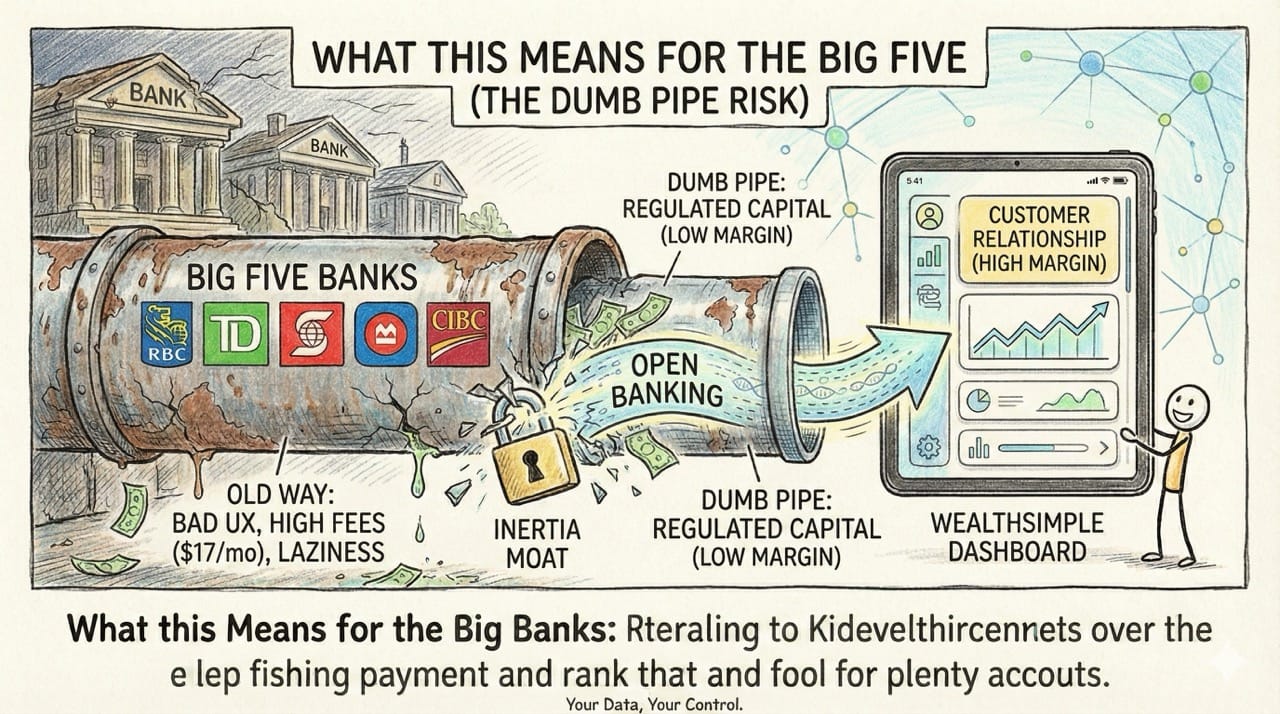

What This Means for the Big Five (The Dumb Pipe Risk)

The Big Five hate this. Their moat is Inertia. They know their UX is bad and their fees are high ($17/month for a chequing account?), but they know you are too lazy to leave.

Open Banking destroys inertia. If Wealthsimple can build a dashboard that sits on top of your RBC account, RBC becomes a "Dumb Pipe." They hold the regulated capital (low margin), while Wealthsimple owns the customer relationship (high margin).

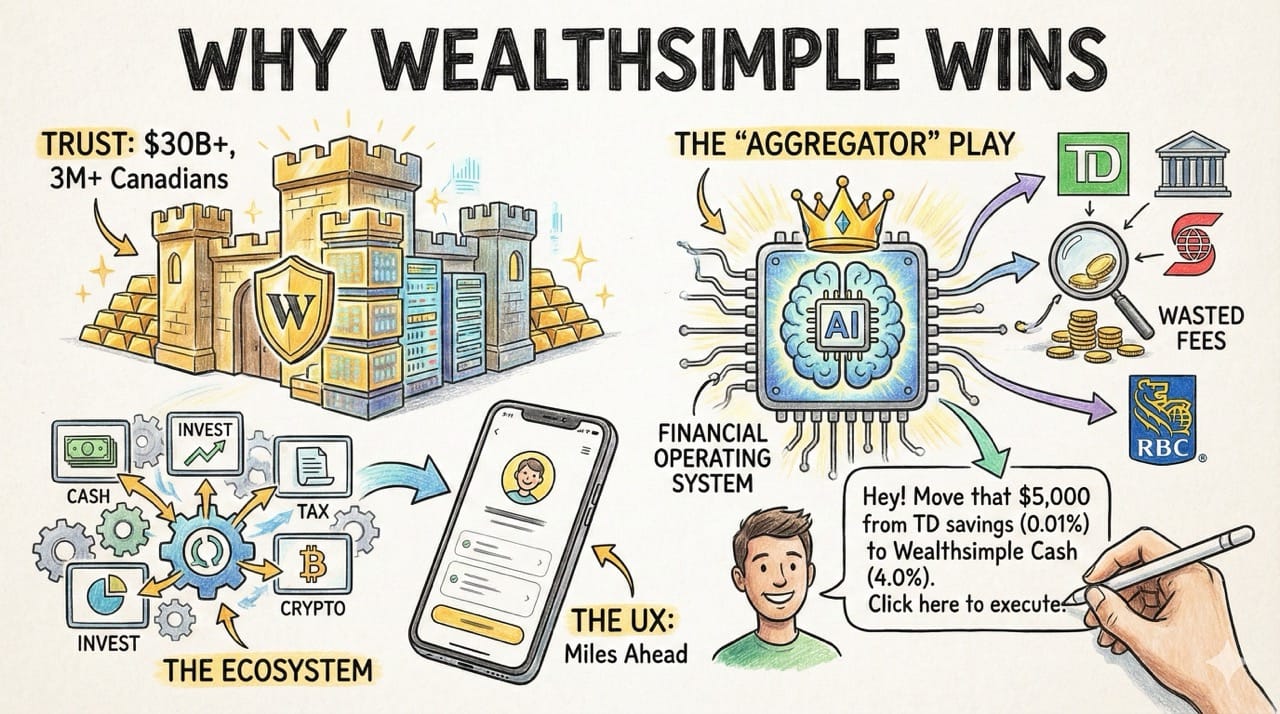

Why Wealthsimple Wins

Wealthsimple is the only player ready for this.

- Trust: They manage $30B+ for 3 million Canadians. They aren't a sketchy startup anymore.

- The Ecosystem: They already have Cash, Invest, Tax, and Crypto.

- The UX: Their app is miles ahead of TD or Scotiabank.

The "Aggregator" Play: Wealthsimple will become the Financial Operating System. You will link your external bank accounts to Wealthsimple. Their AI will analyze your spending, find wasted fees, and say: "Hey, move that $5,000 from your TD savings (0.01%) to Wealthsimple Cash (4.0%). Click here to execute."

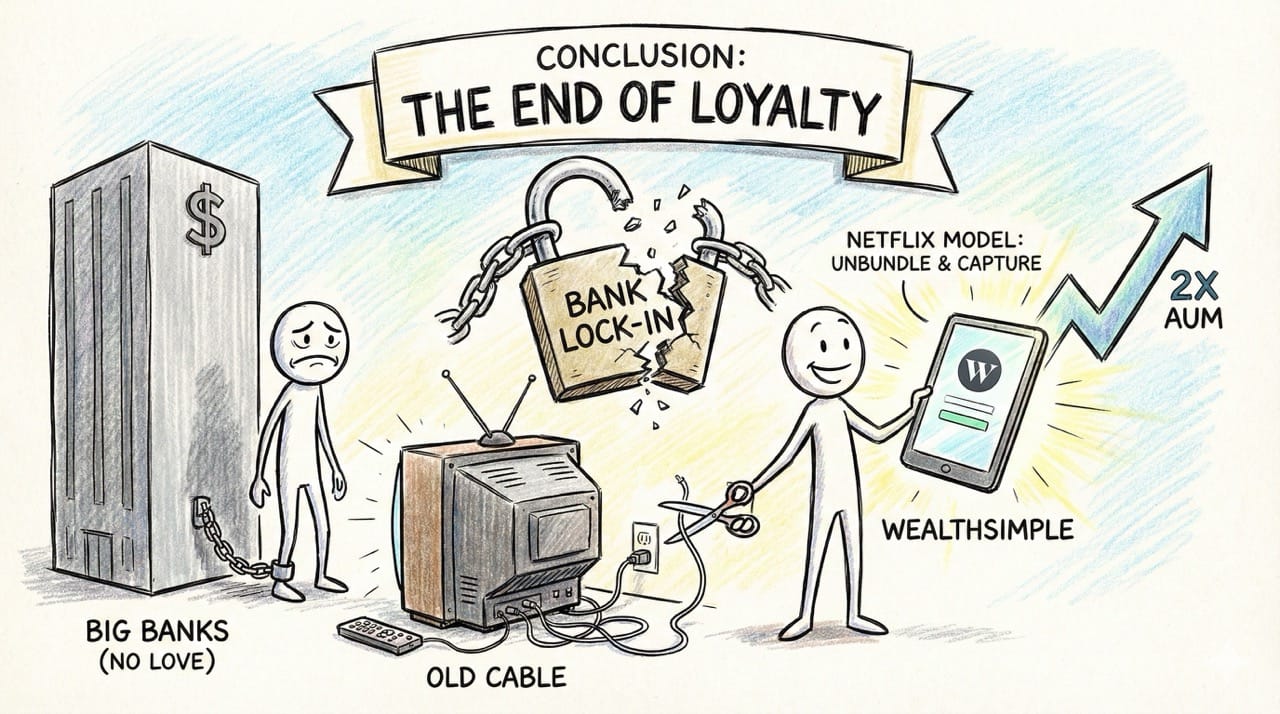

Conclusion: The End of Loyalty

Banking loyalty in Canada wasn't based on love; it was based on lock-in. The lock is broken.

My Prediction: Wealthsimple will double its assets under management (AUM) in 24 months. They will do to Canadian banking what Netflix did to Cable: unbundle the value and capture the attention.