Main Beneficiaries of the GLP-1 Innovations? Insurance Companies.

Ozempic This. Ozempic That.

Inspiration: The Economics of Insurance, Marginal Revolution Podcast.

By the time I am writing this (October 2025), I am going to assume you were not living under the rock and heard about new drugs like Ozempic at least once.

Maybe it was on the news.

Maybe it was at a restaurant, chatting with friends.

Or your favourite celebrity allegedly losing tons of weight thanks to it.

I have multiple trends who are losing a decent amount of weight (body fat, mostly), after years of my intense efforts to get them to eat healthy and exercise more have failed.

So, it is about time I spit some bars about this Miracle Drug.

And, there is no doubt that GLP-1 agonists have taken the news and social media posts by storm.

But what even are they?

Do you eat them? Do you drink them? Heck.. snort them?

Alright, easy there, champ.

What is this Miracle Drug? GLP-1 Ago What?

In short, GLP-1 agonists (not antagonists) mimic the action of a gut hormone.

This does three key things:

- Tells your brain you’re full (reducing appetite).

- Slows your stomach from emptying (increasing that “full” feeling).

- Helps your pancreas release insulin (improving blood sugar).

But… They are not just a “diet drug”.

Landmark studies (such as the SELECT trial for Wegovy) have shown that these drugs dramatically reduce “Major Adverse Cardiovascular Events” (MACE).

This means fewer heart attacks, strokes, and cardiovascular deaths—entirely independent of just the weight loss itself.

Doesn’t that sound too good to be true?

Well, so far, it’s been a magical breakthrough.

Okay, then?

Well, with the current narrative. the media became obsessed with the capital flowing to Novo Nordisk (Ozempic, Wegovy) and Eli Lilly (Mounjaro, Zepbound)…

Basically turning them into trillion-dollar companies (or even more, by the time you are reading this).

The public, employers, and investors see them as a massive new expense.

BUT.. This view is short-sighted.

Sure, the pharma companies are just the first-wave beneficiaries.

They invented the products after all (as a result of tremendous investments in R&D).

But, hear me out.

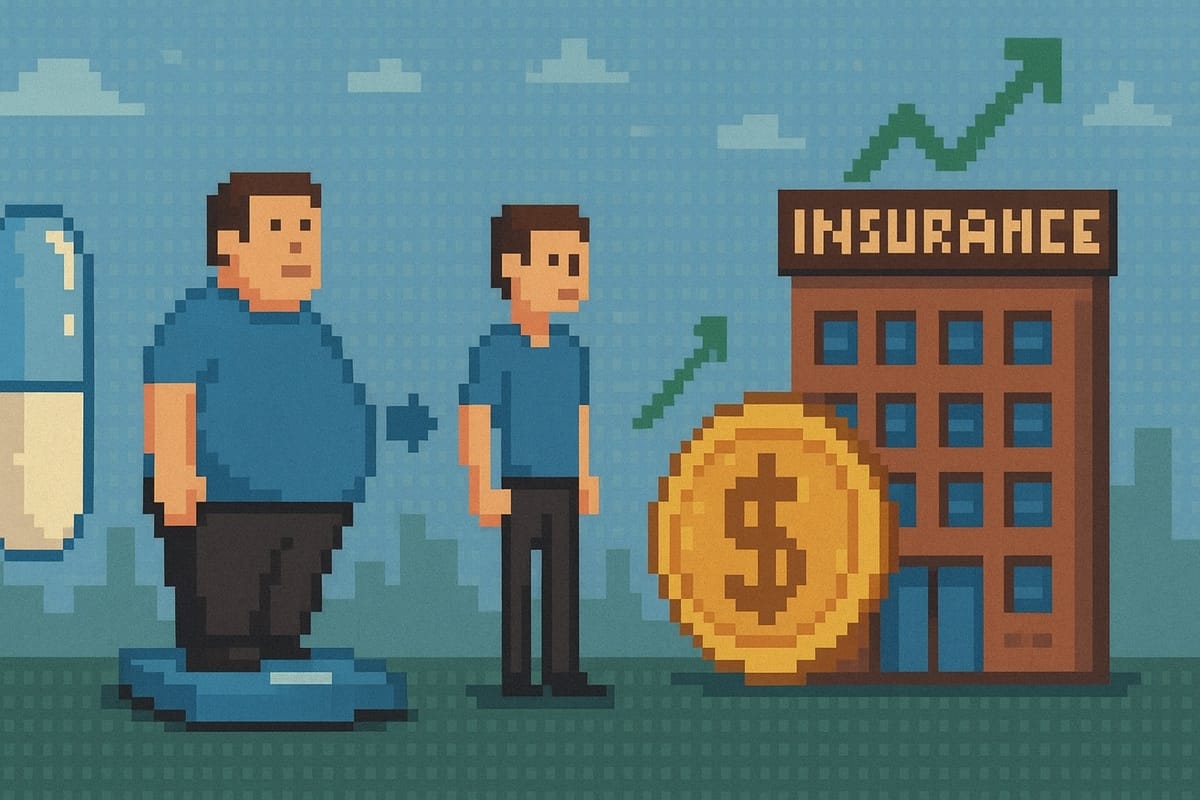

The true, structural, and long-term winners will be the health insurance companies.

They are about to swap a volatile, high-cost liability (obesity co-morbidities) for a fixed, predictable one (the drug cost).

The Short-Term Conflict (The Current “Cost”)

Well, it is no joke.

These drugs are expensive.

(They could be cheaper by the time you are reading this, as David Ricks mentioned the costs should go down over time at All-In Summit.)

But they sometimes list for over $1,000-$1,300 a month in the US.

That’s a hefty change…

Naturally, this has created a massive, immediate financial shock.

Employers and insurers are seeing their pharmacy benefit spending explode.

Because… It technically did, after all?

The current friction (aka the public narrative).

Insurers are creating strict prior authorizations.

They are demanding members prove they “failed” other, cheaper options first.

It doesn’t end there.

Many employers are creating “carve-outs”.

Refusing to cover them for weight loss at all.

The market sees this as proof that the drugs are a burden on insurers. This is the misdirection.

The Long-Term Windfall (The Real Thesis)

Here comes the juicy stuff…

What costs an insurer more than a $15,000/year drug?

- A $60,000 heart bypass surgery.

- A $100,000+ hospitalization and rehabilitation for a major stroke.

- A $90,000/year cost for kidney dialysis, a common result of chronic diabetes.

- A $40,000 knee or hip replacement, often accelerated by obesity.

- Decades of managing Type 2 diabetes (insulin, testing strips, specialist visits, etc.).

You see where I am going with this, right?

So, let’s have a comparison.

The New Math (Fewer Incidents & Payouts)

- The Old Model (High Volatility): Insurers collect premiums and pray they don’t have to pay out for a high number of unpredictable, catastrophic events (surgeries, heart attacks, etc.).

- The New Model (High Predictability): Insurers collect premiums and pay a fixed, predictable monthly cost for GLP-1s. In exchange, their catastrophic event payouts plummet.

The Boost to Profits

This trade is a CFO’s dream.

They are exchanging a volatile, seven-figure liability for a stable, five-figure asset.

They can now accurately model their costs, year over year.

While premiums will rise to cover the “high cost of drugs,” the net profit margin will expand significantly as the much larger, unpredictable surgical and emergency bills vanish from their books.

The Long Game

The current fight over drug coverage is a temporary, short-term budget problem.

The real story is the long-term financial restructuring of the health industry.

So, my friends, don’t be fooled by the current denials.

Insurers are simply stalling while they figure out how to price this new reality into their premiums.

Once the models are set, they will aggressively prefer members to be on these drugs.

What About the Pharma?

Pharma companies get rich for a decade before their patents expire.

The insurance companies, by systematically eliminating their single biggest source of catastrophic claims, will get richer for generations.

A world where we have fewer overweight people, healthier families, and companies profiting more as a win-win-win for society?

Sounds too good to be true? Maybe. Maybe not. We will see.

Until then, please exercise and eat healthy. I believe in you.