Best (Anecdotal) Investments I Had? Following the Money

I used to read balance sheets. Now, I read the guest lists of private dinners.

Inspiration: A throwaway line on the Prof G Podcast about “following the capital, not the earnings,” and realizing that valuations are just feelings with math.

Disclaimer: None of this is financial advice. I am a marketer, not a wealth manager. Do your own research.

I started investing during the COVID era.

Like everyone else, I got sucked in by the GameStop saga. I saw lines going up, and I wanted in.

But I’m a nerd. I didn’t want to just gamble; I wanted to understand why. So, I went deep. I read every book I could find. My favorite was Benjamin Graham’s The Intelligent Investor. I became obsessed with valuations, P/E ratios, and “margin of safety.”

I tried to be a “Value Investor.” I avoided crypto because I couldn’t value it. I tried to find undervalued companies.

And I got burned.

I put a little money into Cathie Wood’s ARK funds early on. I thought I was investing in “innovation.” I learned the hard way that “innovation” without “profit” is just speculation. The downside was brutal.

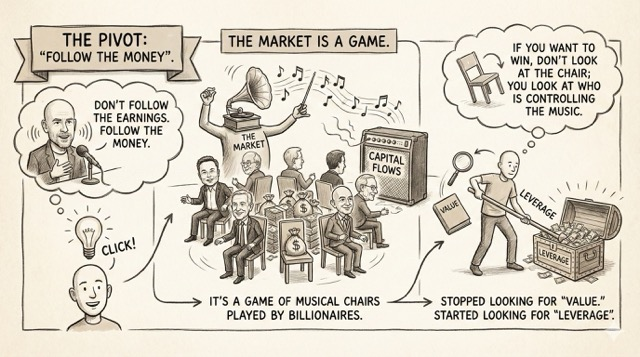

The Pivot: “Follow the Money”

Then, I heard Scott Galloway say something on his podcast: “Don’t follow the earnings. Follow the money.”

It clicked. The market isn’t efficient. It’s a game of musical chairs played by billionaires. If you want to win, you don’t look at the chair; you look at who is controlling the music.

So, I stopped looking for “value.” I started looking for “leverage.”

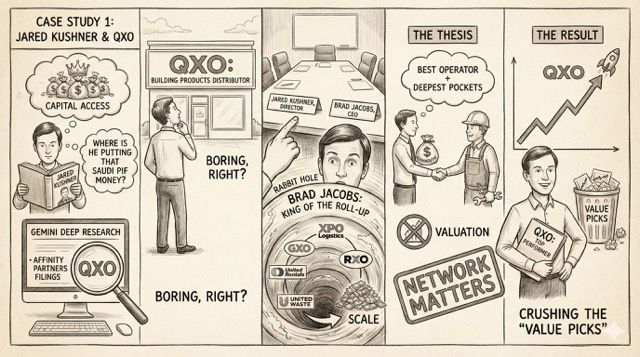

Case Study 1: Jared Kushner & QXO

I read Jared Kushner’s book when it came out. Regardless of politics, it was clear he operates in a different league of capital access.

I got curious. “Where is he putting that Saudi PIF money?”

I fired up Gemini Deep Research. I dug into Affinity Partners’ filings.

I found a weird ticker: QXO.

It wasn’t a tech company. It was a building products distributor. Boring, right?

But then I looked at the board. Jared Kushner was a director. And the CEO? Brad Jacobs.

This sent me down a rabbit hole. Brad Jacobs is the king of the “roll-up.” He built XPO Logistics, GXO, RXO, United Rentals, and United Waste. He takes fragmented industries, buys everyone, and scales to billions.

The Thesis: You have the best operator in history (Jacobs) backed by the deepest pockets in the world (Kushner/PIF). The valuation didn’t matter. The network mattered.

The Result: QXO became one of the best performers in my portfolio, crushing the “value picks” I spent weeks analyzing.

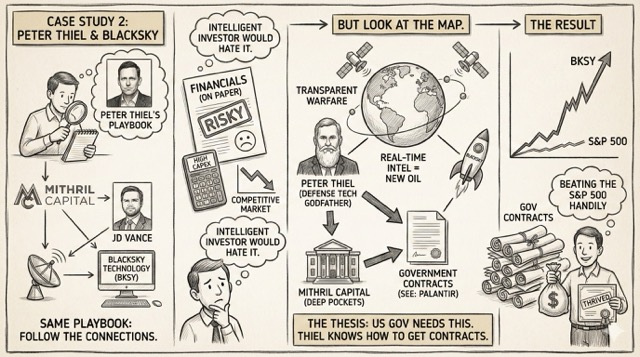

Case Study 2: Peter Thiel & BlackSky

Same playbook. I wanted to see what Peter Thiel was touching.

I researched Mithril Capital (Thiel’s fund). I saw a connection to a guy named JD Vance (long before the VP run).

And I found a company called BlackSky Technology (BKSY).

On paper, it was a risky satellite imagery company. High CapEx, competitive market. The Intelligent Investor would have hated it.

But look at the map.

- Peter Thiel (Defense tech godfather).

- Mithril Capital (Deep pockets).

- The Geopolitics: We are entering a world of transparent warfare. Real-time satellite intelligence is the new oil.

The Thesis: The US government needs this technology, and Peter Thiel knows how to get government contracts (see: Palantir).

The Result: BlackSky didn’t just survive; it thrived on government contracts. The stock appreciated massively, beating the S&P 500 handily.

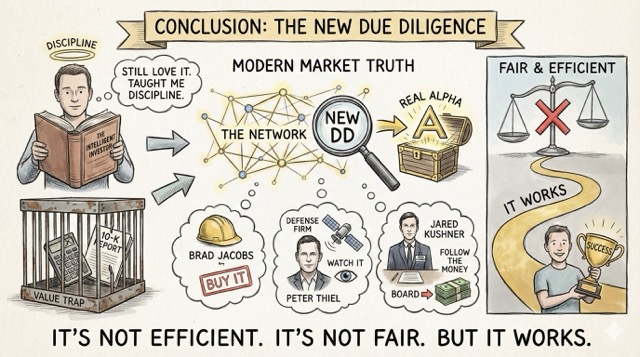

Conclusion: The New Due Diligence

I still love The Intelligent Investor. It taught me discipline.

But in the modern market, “Value” is often a trap. The real alpha isn’t in the 10-K report. It’s in the network.

When Brad Jacobs starts a company, you buy it. When Peter Thiel backs a defense firm, you watch it. When Jared Kushner joins a board, you follow the money.

It’s not efficient. It’s not fair. But it works.